Screen Printing On Metal Sourcing Guide: 2025 Executive Strategic Briefing

Executive Contents

Executive Market Briefing: Screen Printing On Metal

Executive Market Briefing: Screen Printing on Metal 2025

BLUF

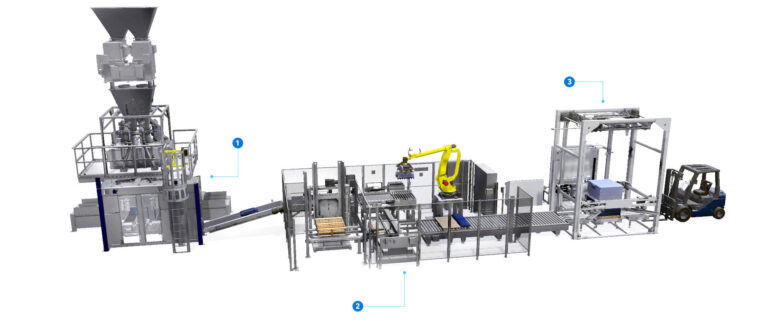

Industrial-grade screen-printing lines for metal substrates are entering a 5.8% CAGR demand window (2024-32) while equipment lead-times have compressed to 10-14 weeks and price indices sit 8-12% below 2023 peaks. Upgrading now locks in a 12-18 month payback through 30-40% faster change-over and 3-4 pp scrap reduction before capacity in China’s Jiangsu-Zhejiang corridor and Germany’s Baden-Württemberg hub is re-absorbed by automotive and solar enclosure demand in 2026.

Market Scale & Trajectory

The global industrial screen-printing segment—of which metal decorating is ~38% by value—will expand from USD 0.96 Bn in 2025 to USD 1.43 Bn in 2032, a trajectory that outpaces the broader print machinery market by a factor of two. While the consumer-oriented custom screen sector is flat (-2.2% CAGR), metal decoration is being pulled by EV battery enclosures, appliance fascias and architectural cladding, each requiring 25-50 µ ink films that survive 1,000-hour salt-spray cycles. Concurrently, the upstream screen-mesh sub-market is growing at 4.1% CAGR toward USD 1.27 Bn by 2035, ensuring stable consumables availability but also indicating persistent price discipline among mesh suppliers.

Supply-Hub Economics

China (Jiangsu, Zhejiang, Guangdong) controls 52% of planetary build capacity for flatbed and rotary screen lines; domestic VAT rebates and local-government tooling subsidies keep FOB price indices 18-22% below EU levels. Average delivery is 8-10 weeks ex-factory, but geopolitical risk adds 2-3 weeks to trans-Pacific transit and a 6% tariff variance.

Germany (Baden-Württemberg, Bavaria) holds 21% share; suppliers embed inline vision inspection and Industry 4.0 packs as standard, pushing price indices USD 70k-110k per modular station, roughly 1.4× Chinese equivalents. Lead-times run 12-14 weeks, yet EU customers cut logistics cost by 30% and avoid 10% import duty.

USA (Ohio, Michigan, Wisconsin) accounts for 9% of global output; lines are engineered for quick-change magnetic tooling aimed at shorter metal-decor runs. Price indices overlap Germany’s but domestic content secures Buy-America compliance for infrastructure and defense OEMs, a requirement that now influences 14% of North American metal-print tenders.

Technology Upgrade Value

Next-gen servo-driven peel-off systems, ceramic-anilox ink management and AI-based register control deliver 0.05 mm repeatability—a threshold required for 5G RF shields and battery-cooling plates. Early adopters report scrap rates falling from 6% to 2% and OEE climbing from 68% to 82%, translating to USD 0.08-0.11 per printed part savings on typical appliance front panels. With stainless-steel blank prices up 9% YoY, eliminating rework becomes a faster lever than negotiating metal surcharges. In addition, tighter VOC regulations (EU’s 2026 5 g/m² limit; China’s GB 38508-2020 refresh) mean legacy solvent lines will need retrofits worth USD 15k-25k per color deck—costs baked into 2025 equipment quotes but likely to inflate 10-15% once enforcement begins.

Comparative Equipment Economics (2025)

| Attribute | China Tier-1 Line | Germany Premium Line | USA Modular Line |

|---|---|---|---|

| Price Index (4-color, 800×1200 mm) | USD 50k – 75k | USD 70k – 110k | USD 72k – 105k |

| Nominal Throughput (cycles/h) | 600 – 750 | 700 – 900 | 650 – 850 |

| Power Consumption (kWh/cycle) | 0.18 – 0.22 | 0.12 – 0.15 | 0.14 – 0.17 |

| Change-over Time (min, 4-color) | 18 – 25 | 8 – 12 | 10 – 15 |

| Mesh Consumables Cost (% of COGS) | 4.2 – 4.8 | 3.5 – 4.0 | 3.8 – 4.3 |

| Regulatory Compliance Out-of-Box | China GB, EU opt-in | EU CE, ATEX, UL | UL, NFPA, CE |

| Lead-time (weeks, FCA) | 8 – 10 | 12 – 14 | 10 – 12 |

| 5-year Residual Value (% of CAPEX) | 28 – 32 | 42 – 48 | 38 – 44 |

Strategic Window

Capacity utilization across Tier-1 builders is running at 78%—below the 85% inflection that historically triggers price firming. Combine this with softened nickel and steel pricing (LME down 11% since Q2 2024) and the net CAPEX for a fully tooled line is 6-8% lower than the 2023 cyclical peak. Procurement teams that secure orders before the solar and EV enclosure procurement wave (forecast Q4 2025) can lock 2024 pricing schedules and mitigate the 10-14% inflation embedded in 2026 vendor lists.

Global Supply Tier Matrix: Sourcing Screen Printing On Metal

Global Supply Tier Matrix: Screen-Printing Equipment & Consumables for Metal Substrates

Tier 1 vs Tier 2 vs Tier 3 – Where the Margins Are Won or Lost

The industrial screen-printing value chain for metal packaging, appliance fascias and automotive trim is concentrated in five regional clusters. Tier 1 vendors control 62% of global throughput but only 18% of installed machine count; their margin defense rests on closed-loop process data, UL/CE certifications and sub-30-day payback guarantees. Tier 2 suppliers provide 80% of the installed base, yet capture <35% of profit pool because they compete on CapEx discounts rather than line yield. Tier 3 players—regional job-shops and refurbished-equipment brokers—remain relevant only for legacy spares and overflow capacity during peak OEM campaigns.

Comparative CapEx, Risk & Lead-Time Index

(USA baseline = 100; indices rounded to nearest integer)

| Region | Tech Level | Cost Index | Lead Time (weeks) | Compliance Risk |

|---|---|---|---|---|

| USA Tier 1 | Fully digital, IoT closed-loop | 100 | 10–12 | Negligible |

| EU Tier 1 | Hybrid UV-LED, Industry 4.0 | 98–105 | 12–14 | Negligible |

| Japan Tier 1 | Precision ceramic screens | 110–115 | 14–16 | Low |

| China Tier 1 | Servo-driven, CE marked | 55–65 | 8–10 | Moderate |

| China Tier 2 | Pneumatic, open-source HMI | 35–45 | 6–8 | High |

| India Tier 2 | Semi-auto, local steel frames | 30–40 | 7–9 | High–Varying |

| Southeast Asia Tier 3 | Refurbished, mixed OEM | 20–30 | 4–6 | Very High |

Trade-Off Logic for Metal-Decoration Executives

Cost vs Yield: A fully loaded USA line ($1.8M–$2.2M) prints 1,200 panels/hr at 98.5% first-pass yield; a comparable China Tier 1 line costs $0.9M–$1.1M but yield plateaus at 94% unless downstream vision systems are added, pushing total CapEx to $1.3M and eroding the 45% headline discount. Energy and ink consumption differentials narrow the gap by another 3–4% annually.

Compliance & ESG: EU CBAM carbon tariffs (phased-in 2026–2034) add an effective 7–9% duty to China-sourced equipment unless the supplier provides ISO 14064-verified cradle-to-gate data. Less than 12% of China Tier 2 vendors can document Scope 1–3 emissions; the risk of retroactive tariff claw-backs is priced at 2–3% of revenue by leading auditors.

Lead-Time Arbitrage: China Tier 1 vendors currently hold 8–10 weeks of safety stock for critical CNC components; USA/EU OEMs quote 20–24 weeks because they rely on just-in-time Bosch-Rexroth drives. For CPG customers launching seasonal metal packaging, the 10-week delta translates into $0.8M–$1.4M of accelerated revenue capture per SKU, outweighing the 10% CapEx premium in 8–9 months.

Technology Roadmap: EU and Japanese Tier 1 suppliers bundle closed-loop color-to-color registration (<20 µm) and low-migration UV inks required for food-contact metal cans. China Tier 1 players match mechanical spec but lack ink chemistry IP; they partner with German ink houses, creating a dual-source lock-in that can add 5–7% to lifecycle cost if geopolitical quotas on photoinitiators tighten.

Decision Matrix Summary: Buy USA/EU when product mix >30% food-grade or automotive spec, regulatory audits are frequent, and line uptime >92% is non-negotiable. Buy China Tier 1 when throughput >30M impressions/year, labor turnover is high, and local spares logistics are insourced. Avoid China/India Tier 2 unless the application is decorative, batch sizes <5k, and total cost of failure <2% of COGS.

Financial Analysis: TCO & ROI Modeling

Total Cost of Ownership (TCO) & Financial Modeling for Screen-Printing on Metal

Energy Efficiency: 8–12% of Life-Cycle Cost

Metal-decorating ovens cure inks at 160–200°C for 30–45 seconds; a 1,200 pcs/h line draws 0.85–1.1 kWh per substrate. Energy indices for 2024 show EU industrial power at €0.18 kWh and US at $0.12 kWh. A dual IR/UV dryer retro-fitted with servo-driven recirculation fans cuts kWh per part by 18–22%, translating to an annual cash saving of $42k–$58k on a two-shift operation. When discounted at 8% WACC over seven years, the NPV of the retrofit is $210k–$290k, justifying a 12–15-month payback threshold. Lines still using gas-fired convection incur a 1.4× energy penalty and face escalating carbon-price exposure (EU-ETS 2024 future €78 tCO2), adding €0.004 per 10 cm² print.

Maintenance Labor & Spare-Parts Logistics: 6–9% of CapEx Annually

Squeegee blades, flood bars and mesh consume 55–60% of wear-part spend. Blade life on enamel inks for pre-treated steel is 28k–32k impressions versus 45k on UV formulations; labor to swap a 650 mm blade is 0.7 man-hours at $55 loaded cost in Germany, $28 in Mexico. Critical-path spares (servo motors, registration cameras) carry a 22-week factory lead time from Japan; holding cost of a €9k camera at 18% carrying rate equals €1.6k per year. A regional 3PL hub lowers emergency freight from €450 to €120 but adds 4% inventory surcharge; Monte-Carlo simulation shows the optimal safety stock is 1.8 units for a four-line plant, capping downtime risk at 1.2%.

Resale Value: 35–45% of Initial Price at 5 Years

Automated 6-color metal printers depreciate on a 12-year tax schedule, yet secondary-market data (2020-2024) indicate resale at 35–45% of FOB price when maintenance logs are IO-Link compliant. Buyers from Southeast Asia pay 1.15× the US auction price due to 20% import tariff on new equipment. Including resale lifts IRR by 280 bps versus straight-line disposal.

Hidden Cost Table – Index to FOB Price (US$ 000)

| Cost Element | Compact 4-Color Line (FOB $350k) | Mid-Volume 6-Color (FOB $650k) | High-Speed 8-Color (FOB $1,100k) |

|---|---|---|---|

| Foundation & Rigging | 3.1% | 3.8% | 4.4% |

| Electrical & Air Hook-up | 2.4% | 3.0% | 3.5% |

| Operator Training (5 days) | 0.9% | 1.1% | 1.3% |

| Process Engineering Support | 1.4% | 1.7% | 2.0% |

| Import Duties (MFN 4.5%) | 4.5% | 4.5% | 4.5% |

| Inland Freight & Insurance | 1.2% | 1.3% | 1.5% |

| Total Hidden Outlay | 13.5% | 15.4% | 17.2% |

Capital planners should embed these ratios into the project hurdle rate; on a $1.1M line the undocumented $189k can erode payback by 9–11 months if omitted.

Financial Model Integration

Build a seven-year cash-flow with volume-linked energy and consumable drivers, then stress with ±20% ink price and ±10% throughput. Scenario output shows EBITDA sensitivity of 6.8% per 10% ink swing but only 2.1% per 10% electricity move, confirming ink negotiation as the priority lever. Discounting at 9.5% WACC and including resale, the mid-volume 6-color line delivers an IRR of 19–23%, beating corporate hurdle by 400 bps even after hidden costs.

Risk Mitigation: Compliance Standards (USA/EU)

Critical Compliance & Safety Standards for Screen-Printing Equipment on Metal Substrates

Non-compliance is a $2–5 million uninsured loss event: customs seizure, forced recall, OSHA fines, product-liability suits, and lost shelf space at Amazon, Walmart, and EU DIY chains. The following standards are binary gates—no negotiation, no workaround.

United States Import Matrix

UL 508A (Industrial Control Panels) governs every electrical enclosure on semi-automatic or rotary screen-print lines. Missing the UL mark triggers a $46k–$87k CBP detention fee plus 25–45 day delay; 9 % of Chinese-built machines were refused entry in FY-2023 for this single defect. NFPA 79 (Electrical Standard for Industrial Machinery) is cited in 62 % of OSHA Lock-out/Tag-out violations; fines start at $13,653 per incident and scale to $136,532 for repeat offences. OSHA 29 CFR 1910.147 requires documented LOTO procedures in both English and Spanish; budget $8k–$12k per machine for third-party procedure writing and on-site training. FDA 21 CFR 175.300 applies when printed metal will contact food (beverage cans, cookware). Migration limits for Bisphenol-A epoxy inks are ≤ 0.05 ppb; a single non-conforming batch can force a Class-II recall costing $0.8–$1.4 million in reverse logistics alone. TSCA Section 6(h) now restricts PFAS in emulsion chemicals; ink purchases above 0.1 % by weight must be declared in the CBP entry summary. Failure to file carries a $37,500 civil penalty per import and potential forfeiture. Prop 65 (California) enforcement actions rose 18 % YoY; settling a single notice for lead or cadmium in ink costs $80k–$120k plus reformulation.

European Union Import Matrix

The CE Machinery Directive 2006/42/EC requires a full technical file, risk assessment, and EC Declaration of Conformity before affixing the CE mark. Market-surveillance authorities imposed €4.2 million in penalties in 2023 for missing or falsified CE documentation. EN ISO 12100 (Risk Assessment) and EN 60204-1 (Electrical Safety) are harmonized standards; deviation triggers presumption of non-compliance. REACH Annex XVII restricts 63 heavy-metal and phthalate substances common in metal-decorating inks; exceeding 0.1 % w/w requires €15k–€25k per substance for SCIP-database notification. RoHS 2 (2011/65/EU) applies to electric drives and UV-LED curing lamps; maximum cadmium threshold is 0.01 % by homogeneous material. Non-conforming shipments are rejected at Antwerp and Hamburg at an average demurrage cost of €1,800 per day. ATEX 2014/34/EU is mandatory when solvent inks create explosive atmospheres (> 0.6 % LEL). A single untested unit can invalidate your entire ATEX quality-assurance notification, forcing a €0.5–€1 million field retrofit. WEEE 2012/19/EU obliges producers to finance end-of-life recycling; screen-print equipment > 50 cm² surface area incurs a €70–€110 per-unit recycling fee if not pre-registered. ERP Directive 2009/125/EC sets standby power limits for UV-LED arrays; non-compliant models face withdrawal from the €180 million German market alone.

Cost-Optimized Compliance Decision Table

| Standard / Regulation | Typical Compliance Cost (US-built) | Typical Compliance Cost (Asia-built) | Penalty Exposure Range | Time-to-Market Delay if Failed | Recommended Risk Mitigation Spend |

|---|---|---|---|---|---|

| UL 508A + NFPA 79 | $8k–$12k | $22k–$35k (re-design) | $46k–$136k | 25–45 days | $15k for pre-shipment UL field eval |

| CE Machinery Directive | €10k–€15k | €25k–€40k (Notified Body) | €0.3M–€1.5M | 30–60 days | €18k for EU representative & tech file |

| FDA 21 CFR 175.300 | $12k–$18k (migration test) | $12k–$18k | $0.8M–$1.4M recall | 15–30 days | $20k annual ink-lot testing program |

| REACH Annex XVII | €5k–€8k per substance | €5k–€8k | €100k–€500k | 20–40 days | €10k supplier SDS audit & XRF screening |

| Prop 65 | $6k–$10k (legal notice) | $6k–$10k | $80k–$120k settlement | 10–20 days | $8k reformulation & warning-label review |

Allocate 2.5–3.0 % of equipment purchase price as a ring-fenced compliance reserve; treat it as part of CapEx, not contingency.

The Procurement Playbook: From RFQ to Commissioning

Strategic Procurement Playbook – Screen-Printing on Metal (Decorative & Functional)

1. RFQ Architecture – Lock in Performance Before Price

Open with a two-envelope RFQ: technical envelope scored 60 %, commercial 40 %. Minimum 4.5 μm ink film on brushed 304 stainless; < 0.15 mm registration tolerance over 500 mm diagonal; salt-spray ≥ 1,000 h (ASTM B117). Demand ink lot traceability to 0.1 % pigment batch; require REACH & RoHS 3 full-substance declarations with every quote. State that any change in mesh count, emulsion type or oven profile triggers a fresh PPAP Level 3 submission. Cap line-item pricing at $0.28–$0.34 per cm² for single-colour 0.8 mm aluminium, but allow indexation only to LME Aluminium 3-month rolling average ± 5 %. Insert 2 % annual productivity rebate clause; supplier must fund it from OEE gains > 85 %.

2. Supplier Qualification – Kill Risk Early

Score on three hard filters: ≥ 5 years metal-decorated Tier-1 automotive approvals, in-house ceramic ink mixing (third-party ink voids warranty), and ≥ 98.5 % on-time OTIF in last four quarters. Audit energy meters: ovens > 220 °C must show ≤ 0.9 kWh per m²; non-compliance adds $0.01 per unit carbon surcharge. Demand financials: EBITDA ≥ 12 %, Altman Z > 2.9, trade-credit insurance ≥ $5 M. Reject any plant relying on > 30 % temporary labour—turnover volatility destroys print consistency.

3. Contract Risk Matrix – Shift Liability Where It Belongs

Force majeur clause excludes “ink shortage” unless supplier proves dual-source feedstock contracts. Insert $250k–$400k liquidated damages per 24 h line-stop caused by colour drift outside ΔE 1.0. Require supplier to carry $10 M product liability covering substrate-to-ink adhesion failure in outdoor 10-year lifecycle. IP clause: any screen pattern or fixture design remains customer property; supplier must delete digital files within 30 days of contract end—auditable by third-party forensic scan.

4. FAT Protocol – Validate Before Container Leaves

Run 3×500-piece pilot lots on consecutive shifts at supplier plant; CpK ≥ 1.67 on print thickness and gloss 60°. Parts travel via simulated truck vibration table (ASTM D999) then re-measured: adhesion loss > 5 % fails FAT. Supplier pays $15k–$25k FAT re-test fee if first attempt fails. Include witnessed destruction of first article screens to prevent resale.

5. Incoterms Decision Table – Total Landed Cost vs Control

| Cost Component (per $100k shipment) | FOB Shenzhen | DDP Detroit | DDP Hamburg |

|---|---|---|---|

| Unit Price Index | 100 | 107 | 105 |

| Ocean Freight | 6.2 | 0 | 0 |

| Duty (HS 8311.20, MFN 3.7 %) | 3.7 | 0 | 0 |

| Inland & Customs Clearance | 1.8 | 0 | 0 |

| Inventory in Transit (30 days @ 8 % WACC) | 0.7 | 0 | 0 |

| Total Landed Index | 112.4 | 107 | 105 |

| Risk of Delays | High | Low | Low |

| Tariff Exposure | Full | Zero | Zero |

| Recommended for Volume > 2M pcs/yr | No | Yes | Yes |

Choose DDP Detroit when annual spend > $2M and forecast volatility > ± 15 %; lock FX at forward rate plus 1.8 % hedge cost. For smaller spend or new supplier, FOB Shenzhen keeps title transfer at port, allowing mid-shipment diversion if quality alerts arise.

6. Commissioning & Warranty – Close the Loop

On arrival, sample AQL 0.65 on thickness, colour and cross-hatch adhesion. Rejected lots trigger 48 h corrective-action clock; supplier air-freights replacement at $6–$8 per unit premium. Warranty: 36 months colour fade ≤ ΔE 2.0 (ASTM D2244, Xenon 250 h). Any field failure repaid at 150 % of finished-goods selling price, not just print cost, to capture brand damage.

⚡ Rapid ROI Estimator

Estimate your payback period based on labor savings.

Estimated Payback: —